FOMC Special: A history of the last tightening cycle

2015 rate hiking cycle; 2018-2019 QT or something like that

It’s no secret we’re quite likely getting a rate hike from the Fed today - Wed, May 4, 2022. Unless we have some kind of an apocalyptic event, we’re probably going to see a straight 50bp (0.50%) increase in the Fed Funds Rate, something we haven’t seen in a long time.

But, what has always been the point of interest is the Quantitative Tightening (QT) plans and we’re meant to hear a decision on that. The last meeting minutes already gave us an indication of what to expect in terms of QT but, none of this has been confirmed.

I thought it might be helpful to run through what we know and a bit of history that may give us some indication of where we stand.

The QT Plan As We Know It

The minutes of March 2022 discussed a possible plan to reduce balance sheet by $95 billion ($60B treasuries + $35B Mortgage-Backed Securities) per month.

They’re discussing a timeframe of 3 months, which works out to just over $1 Trillion reduction in 1 year’s time.

As for the nature of the reduction - much of the treasuries have maturities less than a year and a large proportion can be redeemed at maturity.

The MBS, however, have longer maturities and fewer prepayments (higher rates mean fewer people refinancing mortgages). So, the bulk of these will be “outright sales”. Also given the rising rates, they’re sure to be selling these at a loss.

This is quite aggressive and is sure to send shockwaves through the system. Whether they will ultimately be able to follow through with this plan is another question altogether. It didn’t work so well last time and they had to stop and reverse course.

So, what happened last time?

A Brief History of Rate Increases & QT or something like that

The Fed started the “tightening” cycle by raising rates. That’s always the preferred method.

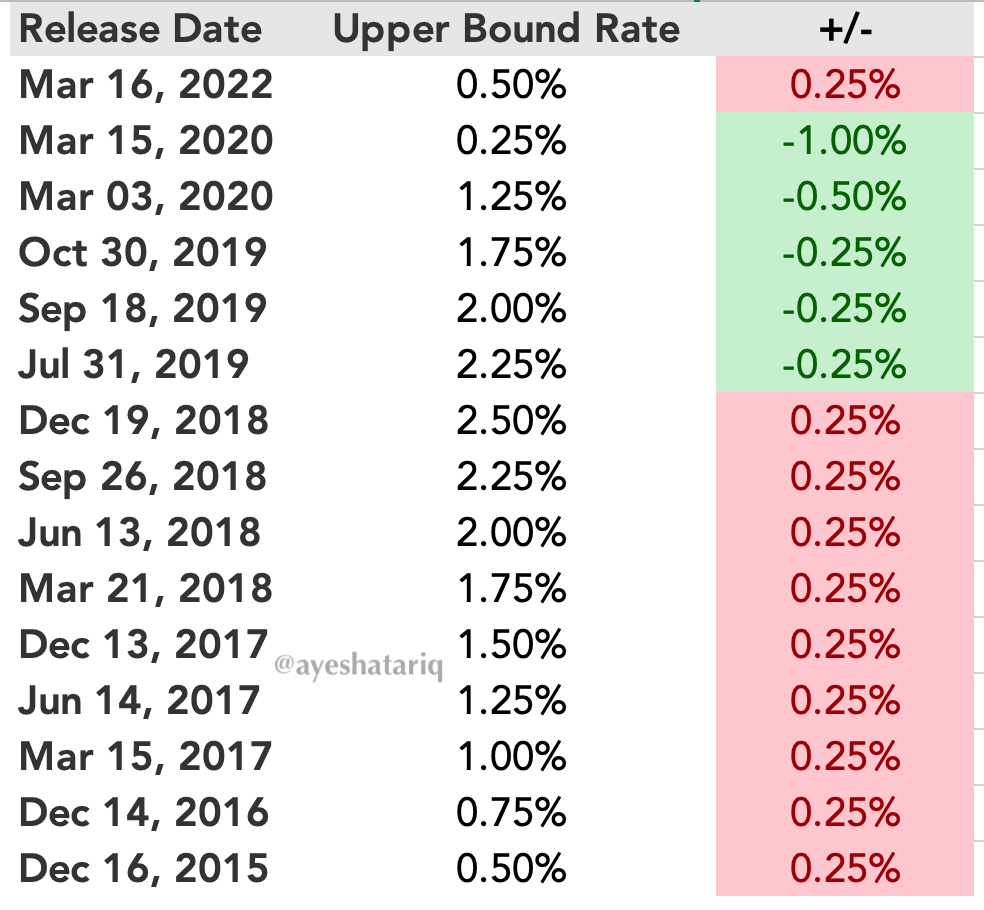

The first rate hike took place in December 2015, starting with a 25bps (0.25%) increase that moved the Fed Funds rate out of the zero bound for the first time in 9 years.

The Fed’s balance sheet hovered around $4.4T in 2015, more than double the amount of what it was coming out of the Great Financial Crisis in 2009.

By the end of 2016, the Fed had hiked rates only by another 0.25% and the balance sheet still hovered around $4.4T.

The Fed had stopped buying bonds at the end of 2014 so throughout the period of 2015 to early 2018, the balance sheet remained largely stable.

On February 05, 2018, Jerome Powell took office as the new Fed Chair and continued to raise rates until the end of 2018.

During the 2018-2019 tightening cycle, the Fed agreed on a maximum of $50B ($30 treasuries + $20MBS) reduction of the balance sheet. It took them up to a year to reach this level, starting out at $10B/month. They reduced almost $650B over the course of 2 years.

By late 2018, early 2019, global growth pressures were mounting. The increase in interest rates and the so-called quantitative tightening had begun putting pressure on both stocks and bond yields.

The Yield Curve started to flatten significantly and the S&P saw a drawdown of almost 20%. The Fed stopped hiking rates with the last hike in Dec 2018.

March 2019, the Yield Curve inverted.

Deflation was becoming an issue and the ECB announced a rate cut in July because of low inflation levels.

By July 2019, the Fed had to take the lead, reversed course and started their first rate cut.

September 2019

On September 16, 2019, the repo rates1 started to spike. Both the Effective Fed Funds Rate (EFFR) and the Secured Overnight Financing Rate (SOFR) started to move outside the the FOMC’s target range. A few basis points is not entirely unusual but these spikes were well above the range.

On September 17, 2019, the SOFR crossed 5% and this is was at a time when the Upper Bound of the Fed Funds Rate was 2.25%. The Fed responded by injecting $75 billion against treasuries and MBS. This operation provided $53 billion in additional reserves and led to an immediate decline in rates.2

The Fed also continued to reduce rates for the rest of the year.

And then the Pandemic hit.

Most argue that the withdrawals for corporate tax season was what led to the situation on Sep 17. In reality, the answer is not so simple.

The excess liquidity in the system had brought about asset bubbles and price bubbles. Fueled with practically free cash, there was a lot speculation in the market.

As the fed started to reduce liquidity in the system, volatility increased. The hedge funds started to play the market with “basis trades3”, and used the repo market to do them. While the Fed bailed them out back in September, the trades of course, later blew up in March 20204.

So in essence, the declining reserves in the system, i.e., decrease in liquidity had a major part to play.5

What’s Different this Time?

Well, for one thing the balance sheet is now massive, at close to $9 Trillion. Prior to the Pandemic, the balance sheet stood at $4.1T.

Inflation has been on a tear. In 2018-2019, the level of inflation was below 3%, whereas now the YoY CPI is 8.5%

Unemployment however, remains at similar levels as earlier, around 4%.

The level of unemployment and inflation were the driving forces that led the Fed to believe that they could successfully implement rate increases and QT.

Final Thoughts: Do We Smell a Recession?

During the last press conference in March 2022, concerns over a recession were dismissed as the Fed’s consensus is that the economy is in a very strong position because of the low unemployment rate. But, we just saw a negative GDP growth number last week at -1.4% for Q1, vs. 6.9% for the prior quarter. This doesn’t bode well for the economy.

There is also a risk that unemployment may spike once, we start to see meaningful tightening in the system.

With the 10Y vs 2Y yields narrowing and inverting over the last couple of weeks the question of a recession doesn’t go away. Raising rates and taking away liquidity from a system that is slowing is the ideal recipe for a recession.

I’ve said this before and I will say it again - the Fed can and will tighten into a recession if they have to. They’ve always believed that they have the policy tools to walk back the situation and they might do it again.

Will they make a policy mistake and break the economy? Who can say at this point. But when you’re staring at a $9 Trillion balance sheet, with inflation soaring, something has to be done.

May the Force be with us!

Repo rate: The rate charged for a Repurchase Agreement. A repurchase agreement, or 'repo', is a short-term agreement to sell securities in order to buy them back at a slightly higher price.

The basis trade is a long-running investment that seeks to exploit pricing gaps between Treasury securities and futures.